In a gobal economy that runs on the assumption that individuals have full access to traditional banking, living without that access has a number of costs. People without access to a bank account are termed as the "unbanked", it is a problem that needs to be solved if we wish to address poverty, equal access, human rights, and improve quality of life.

It is estimated that over a billion people are unbanked, this is most prevalent in Africa, but it effects every country, including America with nearly 16 million US households currently unbanked. Additionally, 16 percent of Americans are considered “underbanked.” This means they have a traditional bank account, but also use alternative financial services, such as payday loans or car title loans.

The Unbanked are forced to pay high fees for everyday financial services like check cashing and money orders. It can cost anywhere from a few dollars to well over $10 to cash a check and up to $2 or more per money order. Utilizing credit is especially challenging for unbanked people. Non-bank credit including buy here, pay here (BHPH) and payday loans charge outrageously high interest fees. Interest rates on BHPH loans can run as high as 20%, and payday loans can charge the equivalent of 400% in interest.

Bank accounts also provide more immediate access to money by supporting direct deposited wages and government checks. Deposits are also often insured and protected against bank closure, plus they pay interest on savings. According to the Financial Health Network, unbanked and underbanked Americans spent $189 billion in fees and interest on alternative financial products in 2018, the latest year for which there is complete data. Using the FDIC’s estimate that some 63 million Americans are unbanked or underbanked, that would be an average of $3,000 in annual costs per person. I used U.S. Data to show this is not just an issue for third world countries, although that is the majority.

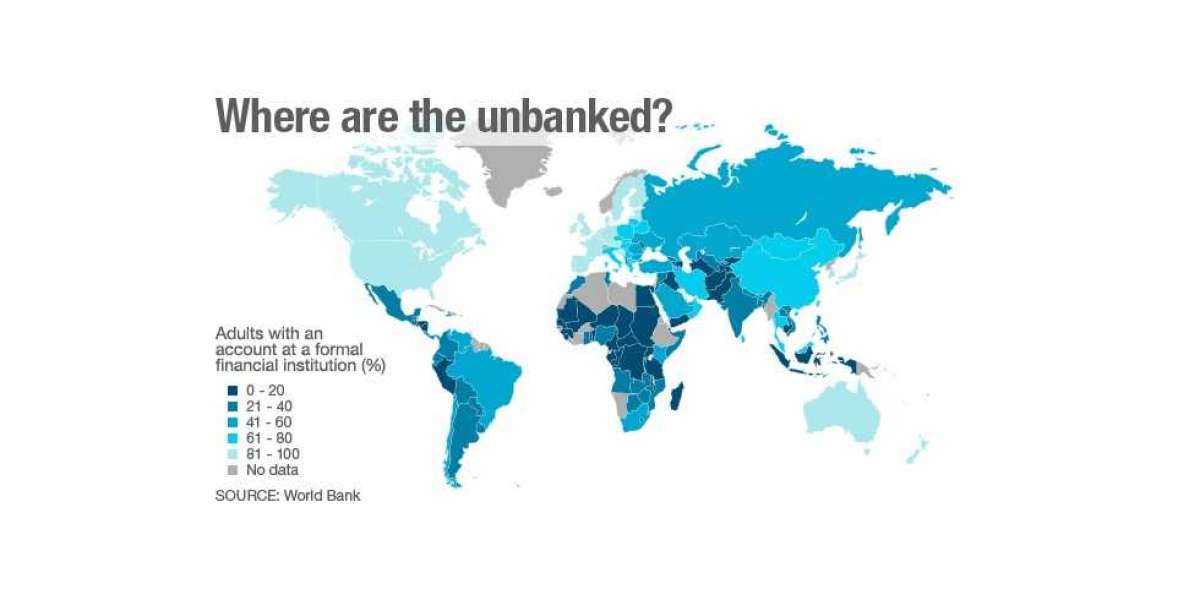

In 2017, the World Bank reported 1.7 billion “unbanked” adults, meaning these individuals did not have “an account at a financial institution or through a mobile money provider.” Although there remain unbanked individuals in developed countries as cited above, most of the unbanked population lives in developing countries. There is a strong link between lacking financial inclusion and living in poverty.

Women account for most of the unbanked. In 2017, about 980 million women did not have a bank account, making up “56% of all unbanked adults globally.” Even in countries with a small percentage of unbanked individuals, women account for most of the unbanked. For example, in Kenya, “where only about a fifth of adults are unbanked, about two-thirds of them are women.” In both India and China, females account for close to 60% of unbanked adults.

China and India have the largest unbanked populations. About 225 million adults in China did not have a bank account in 2017 — the largest unbanked population in a single country. India came in second with 190 million, followed by Pakistan with 100 million and Indonesia with 95 million unbanked people. These four countries, along with Nigeria, Bangladesh and Mexico, accounted for close to 50% of the globe’s unbanked population in 2017. Things are improving but not fast enough.

Providing banking services could lift people out of poverty. World Bank Group President Robert B. Zoellick said that “Providing financial services to the ‘unbanked’ could boost economic growth and opportunity for the world’s [impoverished].” He stated further that “harnessing the power of financial services can really help people to pay for schooling, save for a home or start a small business that can provide jobs for others.” In fact, research shows that “the more [impoverished] people are banking today, the more they are banking on their future[s].”

This brings us to the L.O.V.E. App, it provides anyone, anywhere, with a free bank account. There is no fee to open an account. L.O.V.E. has also integrated upto date technologies such as crypto, and even allows those who have nothing to start with to earn into the platform through participation. By contributing articles (like this blog), users earn Points that can be used (ultimatly) for trading, or exchanged for funds.

L.O.V.E. also offers a marketplace that will expand so people can use this as a tool to earn by offering online classes, goods or services, we even plan to pay users for viewing adds, and sharing other users offerings (affiliate marketing).

One of the main areas where L.O.V.E. can help import wealth to poorer countries is through reduced costs of "Remittances". The World Bank reports that remittance costs an average of 6.3% of the amount sent, cutting prices by a few percentage points can save billiona a year. The aggregate cost of these transfers is now roughly US$30 billion per year. While the direct cost is borne by the migrant senders and their family recipients, there is a sense in which the burden also falls on poor countries as a whole. The reason is that remittances enhance growth in poor countries by providing alternative means for financing investment where transactions costs are high. That is, a means that make remittances easier and cheaper will boost capital formation and productivity in receiving countries.

Remittances, sent for far less, is something L.O.V.E. can offer through inter-user transfers directly on the platform. This means poorer people recieve more, and more capital is infused into their local economies. This is just one of many reasons why L.O.V.E. provides every user with a online bank-account, connected as well with a complete social and commerical media platform.

Financial inclusion is key to the progress of developing economies. It means more investment, business creation, and financial security, with lower transaction fees and greater access to savings and insurance products that help households tackle financial crises. It is the great honor of L.O.V.E. to offer a means for greater financial inclusion to all the unbanked of the world.

John Bush 2 yrs

Nice job Steven